Country Shares of World GDP

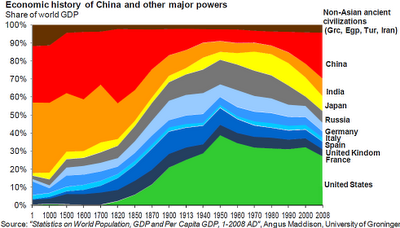

Here's a chart of world GDP, broken down by country share. ( HT: Carpe Diem ). Careful with the x-axis, it is not at all to scale! The basic idea is that India and China had large shares pre-industrial revolution, after which Europe rose. The U.S. shoots up, to over 40% of world GDP by 1950. Then, Japan begins to grow in the 1960s, and China in the 1980s. Suppose countries end up with GDPs proportionate to their populations. What would that picture look like? I've added a bar to the right, showing the break-down of world-population. Look at the U.S. squished down, with less that 400 million out of a world population of over 7,000 million. The biggest change is in the previously un-noticed 'rest of the world". If Africa, the Middle East and so on moved toward freedom, that could be the story of the century. What if they do not? Here's a chart with a new assumption. Suppose the "rest-of-world" does not increase its relative s...