Government Economic Policy

A post at Krazy Economy talks about "austerity" (e.g. in Europe) being a failed program and says that production and freedom are the key. I agree. Do not listen to those who are overly shrill about government money-printing or government deficits. Printing and deficits are bad, but freedom is more fundamentally important to an economy.

One way to classify a government's economic intervention is: structural, fiscal and monetary.

Fiscal policy: What fraction of GDP is spent by the government? On what is it spent? What is the structure of taxes? Do taxes pay for spending, or does the government owe debt?

Fiscal policy: What fraction of GDP is spent by the government? On what is it spent? What is the structure of taxes? Do taxes pay for spending, or does the government owe debt?

One way to classify a government's economic intervention is: structural, fiscal and monetary.

Structural policy and laws: Does the law recognize property rights or is the country communist? Do the courts enforce such rights or are they slow and corrupt? Are owners burdened by regulations on the use of their property: environmental laws, zoning laws, minimum wages, unions, protectionism?

Fiscal policy: What fraction of GDP is spent by the government? On what is it spent? What is the structure of taxes? Do taxes pay for spending, or does the government owe debt?

Fiscal policy: What fraction of GDP is spent by the government? On what is it spent? What is the structure of taxes? Do taxes pay for spending, or does the government owe debt?

Monetary policy: Does the government use fiat money (always "yes" these days)? Does the money supply grow slowly or rapidly?

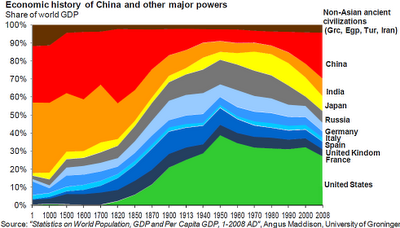

Economics is born on a Freedom Platform: Classical economists like Adam Smith argued for more individual decision making, setting people free from structural constraints like protectionism, rationing, and government price-fixing. The West adopted many of their prescriptions with great success. More recently, Taiwan, South Korean, China and India have shown that structural changes -- increased freedom -- can do wonders for an economy. (Also see de Soto's main thesis.)

Weeds of intervention never rooted out: Unfortunately, alongside their better arguments, some classical economists -- like Ricardo and John Stuart Mills -- were laying the foundation for more government intervention and wealth-redistribution. The climax of these ideas came in the form of the Russian revolution. In the U.S., it came in the form of FDR's NRA, from American intellectuals who -- rejecting the invisible hand -- thought the Soviet system would surpass the U.S.

Fiscal policy ascendant: The NRA was struck down by the SCOTUS. This meant that U.S. government intervention would have to come in drips over decades instead of on fell swoop. Instead, John Maynard Keynes was the flavor of the decades to follow, pretending to rescue Capitalism, not undermine it. Politicians did not need to apologize for spending; deficits bring prosperity! Until: "We're all Keynesian now".

Monetarists bring back Adam Smith: Keynes's ideas brought no prosperity, only rising prices, while government intervention continued relentlessly. The tide shifted to the ideas made popular by Milton Friedman. (Hayek's work had influence here, though it was less "pop".) Though he was a monetarist to other economists, his contribution to the lay-public was to popularize older classical ideas: having individuals Free to Choose. This was a revival of Adam Smith, flaws and all.

Monetarism itself is flawed: Friedman said, "Inflation is always and everywhere a monetary phenomenon." This is does not speak to more fundamental causes. I prefer John Hussman's formulation: "... ... significant inflation is ultimately not a monetary phenomenon as much as it is a fiscal one." Though many detailed theories and prescriptions of the monetarists are wrong, they did call for monetary discipline, and -- by implication -- for fiscal discipline, both of which are good things.

Deregulation: More important than monetary and fiscal discipline was the resurgence of classical ideas about free-markets. Nixon started to toss in the towel on Keynes. Even Carter started to deregulate. Finally, deregulation became the buzzword, climaxing under Thatcher and Reagan. The "Asian Tigers" bought in, and China followed a decade later, with India finally waking up too.

Supply-side spin: For all the talk of "supply side"and tax-cuts from pop-economists like Larry Kudlow, I suspect history will show that Reagan's real contribution was to popularize an ideology of deregulation, small-government, union-busting and privatization. The same with Thatcher.

Partial freedom: Partial "deregulation" can be disastrous. Witness California's attempt to "deregulate" the power industries, by imposing various regulations inspired by another Chicago-school economist, Frank Knight, and faulty ideas like "perfect competition". The biggest blow-up came the housing crisis, where the government had created a facade of a free-market (GSEs like Fannie and Freddie were privately owned, with stocks trading on the market, and banks were freed from Glass-Stegall), when the reality was that the government was implicitly guaranteeing GSE debt, and the Feds and the FDIC were underwriting banks and even hedge-funds (e.g. LTCM). [The "socialization" of risk and failure.]

Statism resurgent: After two stock-market downturns, it is not surprising that public mood -- typically informed by superficiality -- has swung against deregulation and Capitalism. Obama's anti-business rhetoric has found fertile ground. Both Bush and Obama responded with "borrow-and-spend", and that has come to naught. The Fed's response has been to "push on a string" with lower interest rates, and that has come to naught in the face of credit-deflation.

Austerity is not bad, just insufficient on its own: Of course austerity is a good thing if it means not printing money, and living within one's means. Further, when austerity is forced on a country, it can force structural change -- as increased freedom may be seen as the only practical and politically-viable solution. There are many examples of the World bank forcing austerity on a country. There are instances -- as in India -- where this caused the first erosion of statism that had grown for decades. Austerity can be good; freedom is more fundamental. We don't want North Korean style austerity!

Austerity in the U.S.: Despite the Federal stimulus, there has been some austerity in the U.S., with welcome effects. School districts, libraries and cities have cut back. Pension schemes are under scrutiny. Not enough being done? It might seem that way, but this is how change comes: with a fight (witness the recall campaign against Governor Walker in Wisconsin.) When re-distribution schemes are rolled back, recipients will fight even if they know the scheme is unsustainable. This is how groups negotiate in democracies.

Real Hope and Change: Freedom brings prosperity, and prosperity wipes out past sins. The huge WW-II debt -to-GDP burden in the U.S. was erased because GDP grew faster than debt. The U.S. must undo regulations if it is to grow and work off its debt. When Obama wanted to stop Boeing from building a plant in South Carolina, he was fighting to keep some wealth-redistribution in place. Banning a project like the Keystone pipeline is pointless, suicidal lunacy. The U.S. is seeing a boom in energy production -- in both oil and gas. The government does not need to invest in this. It just needs to get out of the way. It just needs to allow people to get on with the business of production. The U.S. actually has the potential to reverse the outflow of manufacturing jobs to China. With more capital intensive production, a narrowing gap in real wages, lower transport costs, and cheap energy, the U.S. could become more competitive. Giving people freedom in their choices of healthcare would lower the one cost that threatens to run up our debt more than any other.

Our choices: Obama has nothing to offer here: he can only scold and complain. He is an anachronistic and clueless loser. Unfortunately, the GOP's nominee -- Romney -- does not show much intellectual leadership either. Still, these two are simply effects -- thrown up by voter opinion. We voters are the cause behind these politicians. If we voters can see our way to sanity and freedom, success is easy. The only things holding the U.S. back are the self-imposed shackles that voters have asked for over the years.

P.S. From Italy (Aug 2013) comes a story of an entrepreneur secretly packing up his factory and shipping it to Poland, to get away from Italian law and high italian labor costs. While economists debate about fiscal versus monetary policy, they give short shrift to structural reform.

Economics is born on a Freedom Platform: Classical economists like Adam Smith argued for more individual decision making, setting people free from structural constraints like protectionism, rationing, and government price-fixing. The West adopted many of their prescriptions with great success. More recently, Taiwan, South Korean, China and India have shown that structural changes -- increased freedom -- can do wonders for an economy. (Also see de Soto's main thesis.)

Weeds of intervention never rooted out: Unfortunately, alongside their better arguments, some classical economists -- like Ricardo and John Stuart Mills -- were laying the foundation for more government intervention and wealth-redistribution. The climax of these ideas came in the form of the Russian revolution. In the U.S., it came in the form of FDR's NRA, from American intellectuals who -- rejecting the invisible hand -- thought the Soviet system would surpass the U.S.

Fiscal policy ascendant: The NRA was struck down by the SCOTUS. This meant that U.S. government intervention would have to come in drips over decades instead of on fell swoop. Instead, John Maynard Keynes was the flavor of the decades to follow, pretending to rescue Capitalism, not undermine it. Politicians did not need to apologize for spending; deficits bring prosperity! Until: "We're all Keynesian now".

Monetarists bring back Adam Smith: Keynes's ideas brought no prosperity, only rising prices, while government intervention continued relentlessly. The tide shifted to the ideas made popular by Milton Friedman. (Hayek's work had influence here, though it was less "pop".) Though he was a monetarist to other economists, his contribution to the lay-public was to popularize older classical ideas: having individuals Free to Choose. This was a revival of Adam Smith, flaws and all.

Monetarism itself is flawed: Friedman said, "Inflation is always and everywhere a monetary phenomenon." This is does not speak to more fundamental causes. I prefer John Hussman's formulation: "... ... significant inflation is ultimately not a monetary phenomenon as much as it is a fiscal one." Though many detailed theories and prescriptions of the monetarists are wrong, they did call for monetary discipline, and -- by implication -- for fiscal discipline, both of which are good things.

Deregulation: More important than monetary and fiscal discipline was the resurgence of classical ideas about free-markets. Nixon started to toss in the towel on Keynes. Even Carter started to deregulate. Finally, deregulation became the buzzword, climaxing under Thatcher and Reagan. The "Asian Tigers" bought in, and China followed a decade later, with India finally waking up too.

Supply-side spin: For all the talk of "supply side"and tax-cuts from pop-economists like Larry Kudlow, I suspect history will show that Reagan's real contribution was to popularize an ideology of deregulation, small-government, union-busting and privatization. The same with Thatcher.

Partial freedom: Partial "deregulation" can be disastrous. Witness California's attempt to "deregulate" the power industries, by imposing various regulations inspired by another Chicago-school economist, Frank Knight, and faulty ideas like "perfect competition". The biggest blow-up came the housing crisis, where the government had created a facade of a free-market (GSEs like Fannie and Freddie were privately owned, with stocks trading on the market, and banks were freed from Glass-Stegall), when the reality was that the government was implicitly guaranteeing GSE debt, and the Feds and the FDIC were underwriting banks and even hedge-funds (e.g. LTCM). [The "socialization" of risk and failure.]

Statism resurgent: After two stock-market downturns, it is not surprising that public mood -- typically informed by superficiality -- has swung against deregulation and Capitalism. Obama's anti-business rhetoric has found fertile ground. Both Bush and Obama responded with "borrow-and-spend", and that has come to naught. The Fed's response has been to "push on a string" with lower interest rates, and that has come to naught in the face of credit-deflation.

Austerity is not bad, just insufficient on its own: Of course austerity is a good thing if it means not printing money, and living within one's means. Further, when austerity is forced on a country, it can force structural change -- as increased freedom may be seen as the only practical and politically-viable solution. There are many examples of the World bank forcing austerity on a country. There are instances -- as in India -- where this caused the first erosion of statism that had grown for decades. Austerity can be good; freedom is more fundamental. We don't want North Korean style austerity!

Austerity in the U.S.: Despite the Federal stimulus, there has been some austerity in the U.S., with welcome effects. School districts, libraries and cities have cut back. Pension schemes are under scrutiny. Not enough being done? It might seem that way, but this is how change comes: with a fight (witness the recall campaign against Governor Walker in Wisconsin.) When re-distribution schemes are rolled back, recipients will fight even if they know the scheme is unsustainable. This is how groups negotiate in democracies.

Real Hope and Change: Freedom brings prosperity, and prosperity wipes out past sins. The huge WW-II debt -to-GDP burden in the U.S. was erased because GDP grew faster than debt. The U.S. must undo regulations if it is to grow and work off its debt. When Obama wanted to stop Boeing from building a plant in South Carolina, he was fighting to keep some wealth-redistribution in place. Banning a project like the Keystone pipeline is pointless, suicidal lunacy. The U.S. is seeing a boom in energy production -- in both oil and gas. The government does not need to invest in this. It just needs to get out of the way. It just needs to allow people to get on with the business of production. The U.S. actually has the potential to reverse the outflow of manufacturing jobs to China. With more capital intensive production, a narrowing gap in real wages, lower transport costs, and cheap energy, the U.S. could become more competitive. Giving people freedom in their choices of healthcare would lower the one cost that threatens to run up our debt more than any other.

Our choices: Obama has nothing to offer here: he can only scold and complain. He is an anachronistic and clueless loser. Unfortunately, the GOP's nominee -- Romney -- does not show much intellectual leadership either. Still, these two are simply effects -- thrown up by voter opinion. We voters are the cause behind these politicians. If we voters can see our way to sanity and freedom, success is easy. The only things holding the U.S. back are the self-imposed shackles that voters have asked for over the years.

P.S. From Italy (Aug 2013) comes a story of an entrepreneur secretly packing up his factory and shipping it to Poland, to get away from Italian law and high italian labor costs. While economists debate about fiscal versus monetary policy, they give short shrift to structural reform.

Comments

Post a Comment