Don't expect QE3 to send prices shooting up

QE3: The Fed just announced a larger-than-expected, and open-ended "QE3". Do not expect significantly higher price-rises in the medium term (at least the next few years). Definitely do not expect hyper-inflation.

Most people who predict hyperinflation use some variant of the "Linear Quantity Theory of Money" and the concept of a banking "Multiplier". Both these ideas are false (except in a fuzzy, informal way). [Ludwig von Mises criticized the Linear Quantity Theory of Money, but many Austrian-sympathizers still continue to apply it.]

The typical interpretation of the Quantity Theory of Money takes the view that there are two important aggregates: on the one hand, there is money; and, on the other hand there are goods traded... with other factors staying mostly constant over the short-run. This model leads people to think: more money is being created, so prices of goods will go up.

Money vs. Goods: There are issues with both sides of the Quantity-Theory equation. On the money side, credit may not increase even if money is "printed". Credit is an important money-substitute. It is a driving force in modern economies because it is huge in the aggregate. Bottom line: the Fed can create money, but it cannot force people to take out loans. On the goods side, as the Austrians have long explained, even if new money is created and goes into goods, it does not go into all goods evenly. Also, it does not have to go into consumption-goods. This was pretty clear during the housing boom: prices of homes were shooting up while prices of many day-to-day goods were rising slowly. The same thing happens in a credit-driven stock-market boom.

Monetary booms often result in deflation: Reinhart and Rogoff have explored financial/banking crises where governments responded with monetary stimulus, lower rates, and credit creation. There are historical precedents where this leads to very high price-rises, but other cases (slightly more numerous) where this has led to a boost to asset prices only, followed by a second bust in asset prices. With this, one sees write-downs on loans related to those assets: credit-deflation, unemployment and tame consumer-prices.

Reading recommendation: There's a new paper on the Dallas Fed site: Ultra-Easy Monetary Policy and the Law of Unintended Consequences - by William White. It is not light reading, but if you print out all 40 pages and give it a few hours of focus, it's a breeze. Very well argued and even if you disagree with parts of it, it will leave you richer.

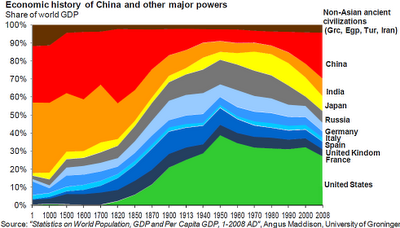

Prices today: At this point, it seems that prices of regular day-to-day goods -- food, energy, housing and health-care -- will not rise much above their historical norm (3% - 5% p.a.). However, low interest rates on "safe" assets are pushing the marginal savings into stocks. So, that is one place where we see an asset boom. Precious metals like gold and silver are good in times of uncertainty: these can shoot up in times of fear-driven deflation just as they can in times of high inflation. This seems ridiculous if one believes the Linear Quantity Theory of Money. However, hugely deflationary episodes often come by a bust of an asset bubble. After an initial shock, people start to look for alternate assets -- like precious metals. [Aside: Of course, there is also a "goods/usage demand" for gold and silver, which can move in the opposite direction if Indians start making a virtue of cutting back on their trousseau's gold content.] Other commodities -- like copper or oil -- are not primarily seen as stores of value; so, I doubt these will shoot sky high unless China pulls off what appears to be impossible. [Bombing Iran could hit oil prices.]

Gold as a standard: If you measure the value of a dollar by using gold alone, I am not predicting a stable dollar. However, if you measure the value of a dollar by the day-to-day food, gas, apartments, homes, cars and computers it can buy, do not expect the dollar to fall much more rapidly in the next few years as a result of QE3.

Caveat Emptor: Obviously these are all just best guesses. How these things unravel is mostly a political question. This means we can predict it only the way we can predict history: where we can almost never predict a major turning point when a large proportion of the populace is convinced that they have to change direction.

Most people who predict hyperinflation use some variant of the "Linear Quantity Theory of Money" and the concept of a banking "Multiplier". Both these ideas are false (except in a fuzzy, informal way). [Ludwig von Mises criticized the Linear Quantity Theory of Money, but many Austrian-sympathizers still continue to apply it.]

The typical interpretation of the Quantity Theory of Money takes the view that there are two important aggregates: on the one hand, there is money; and, on the other hand there are goods traded... with other factors staying mostly constant over the short-run. This model leads people to think: more money is being created, so prices of goods will go up.

Money vs. Goods: There are issues with both sides of the Quantity-Theory equation. On the money side, credit may not increase even if money is "printed". Credit is an important money-substitute. It is a driving force in modern economies because it is huge in the aggregate. Bottom line: the Fed can create money, but it cannot force people to take out loans. On the goods side, as the Austrians have long explained, even if new money is created and goes into goods, it does not go into all goods evenly. Also, it does not have to go into consumption-goods. This was pretty clear during the housing boom: prices of homes were shooting up while prices of many day-to-day goods were rising slowly. The same thing happens in a credit-driven stock-market boom.

Monetary booms often result in deflation: Reinhart and Rogoff have explored financial/banking crises where governments responded with monetary stimulus, lower rates, and credit creation. There are historical precedents where this leads to very high price-rises, but other cases (slightly more numerous) where this has led to a boost to asset prices only, followed by a second bust in asset prices. With this, one sees write-downs on loans related to those assets: credit-deflation, unemployment and tame consumer-prices.

Reading recommendation: There's a new paper on the Dallas Fed site: Ultra-Easy Monetary Policy and the Law of Unintended Consequences - by William White. It is not light reading, but if you print out all 40 pages and give it a few hours of focus, it's a breeze. Very well argued and even if you disagree with parts of it, it will leave you richer.

Prices today: At this point, it seems that prices of regular day-to-day goods -- food, energy, housing and health-care -- will not rise much above their historical norm (3% - 5% p.a.). However, low interest rates on "safe" assets are pushing the marginal savings into stocks. So, that is one place where we see an asset boom. Precious metals like gold and silver are good in times of uncertainty: these can shoot up in times of fear-driven deflation just as they can in times of high inflation. This seems ridiculous if one believes the Linear Quantity Theory of Money. However, hugely deflationary episodes often come by a bust of an asset bubble. After an initial shock, people start to look for alternate assets -- like precious metals. [Aside: Of course, there is also a "goods/usage demand" for gold and silver, which can move in the opposite direction if Indians start making a virtue of cutting back on their trousseau's gold content.] Other commodities -- like copper or oil -- are not primarily seen as stores of value; so, I doubt these will shoot sky high unless China pulls off what appears to be impossible. [Bombing Iran could hit oil prices.]

Gold as a standard: If you measure the value of a dollar by using gold alone, I am not predicting a stable dollar. However, if you measure the value of a dollar by the day-to-day food, gas, apartments, homes, cars and computers it can buy, do not expect the dollar to fall much more rapidly in the next few years as a result of QE3.

Caveat Emptor: Obviously these are all just best guesses. How these things unravel is mostly a political question. This means we can predict it only the way we can predict history: where we can almost never predict a major turning point when a large proportion of the populace is convinced that they have to change direction.

Comments

Post a Comment