How're we doing? (A review of 2014)

Overview: Like last year, 2014 gave us a slowly improving economy, and a rocketing stock market! Since the 2007-08 downturn, most measures of the economy have stabilized and have started to improve from their bottom. Even total-employment got back, though the more important number (Employment-to-population) is still low. The broadest GDP measure has been increasing very slowly. House-prices came well off their bottom, someway half-way to the old peak, but have recently flattened for a few months. Meanwhile, the stock market is at an all-time high.

Corporate profits are high since GDP is growing slowly while firms have kept a reign on costs. Companies have kept buying back stock at above-average levels. This is different from the type of excitement that drove the dot.com boom, because it does not cascade into higher salaries and expenditures: quite the opposite. In the short/medium term, this is "blah" for employment numbers and wages.

Here are some of the details:

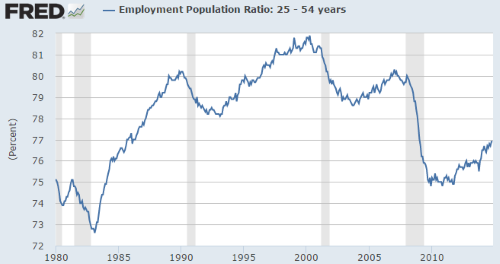

Employment: After seeming to flatten last year, the Employment-to-population ratio jumped up by a percentage point. If we define recessions by level rather than by direction, and if we use this single measure, then we are still in a recession.

Employment: After seeming to flatten last year, the Employment-to-population ratio jumped up by a percentage point. If we define recessions by level rather than by direction, and if we use this single measure, then we are still in a recession.

This measure is closely related to why people still don't think things are fine.

Real GDP per Capita: Real GDP per-capita picked up after seeming to flatten last year.

2014 was a bit better than 2013 and what looked like a flattening now looks like a resumed (though slower) trend.

Home prices: The Case-Schiller index has been rising for two years now.

Price-rise: The 10-year CPI expectation (using TIPS spreads) dropped under 2% almost to 1.5% [Which means that anyone who thinks the official CPI will actually rise much more than this over 10 years should buy TIPS.]

Price-rise: The 10-year CPI expectation (using TIPS spreads) dropped under 2% almost to 1.5% [Which means that anyone who thinks the official CPI will actually rise much more than this over 10 years should buy TIPS.]

This probably reflects the generally low interest rates on US government debt as the dollar has been one of the strongest relative to other currencies.

Stock market: The stock-market is on a "what me worry?" tear. Rumors of its death appear to have been discredited. But that's how stock markets are: up, until they aren't.

Stock market: The stock-market is on a "what me worry?" tear. Rumors of its death appear to have been discredited. But that's how stock markets are: up, until they aren't.

In terms of months and level, it is looking long in the tooth, but history also says it is probably pointless to jump out.

Summary: There is a bit more enthusiasm about the economy, but not much. Lower gas prices will lower the GDP metric directly, but Christmas-related buying will probably improve to compensate. No great improvement is expected and, consequently, companies are unlikely to raise hiring or wages much more than they've been doing. Government entities aren't likely to go gang-busters either, but here too voters are a little more willing to approve funding for roads and schools. A "new normal" seems like a good guess: growth, but slow.

Even though the stock-market is booming, it is without excitement: more like "there's no other game in town, while the FED keeps rates low; and, profits are high through cost-control". The divergence cannot go on forever, but it can resolve itself in various ways. Much of the market-sentiment is driven by what John Hussman calls "superstition" about the Fed's ability to keep this playing out for a many more years. The FED continued to say that the turning point is far away, so the game could go on.

The biggest "anticipated wildcards" for 2015 will how the market reacts to the FED, and how the drop in oil-prices filters through (given that a lot of capital investment and employment growth came from the U.S. oil sector). A new downturn -- particularly in the stock market, if not the economy -- is likely before Obama's term ends, but he might squeeze through... and Democrats will have something to brag about.

Corporate profits are high since GDP is growing slowly while firms have kept a reign on costs. Companies have kept buying back stock at above-average levels. This is different from the type of excitement that drove the dot.com boom, because it does not cascade into higher salaries and expenditures: quite the opposite. In the short/medium term, this is "blah" for employment numbers and wages.

Here are some of the details:

Employment: After seeming to flatten last year, the Employment-to-population ratio jumped up by a percentage point. If we define recessions by level rather than by direction, and if we use this single measure, then we are still in a recession.This measure is closely related to why people still don't think things are fine.

Real GDP per Capita: Real GDP per-capita picked up after seeming to flatten last year.

2014 was a bit better than 2013 and what looked like a flattening now looks like a resumed (though slower) trend.

Home prices: The Case-Schiller index has been rising for two years now.

Price-rise: The 10-year CPI expectation (using TIPS spreads) dropped under 2% almost to 1.5% [Which means that anyone who thinks the official CPI will actually rise much more than this over 10 years should buy TIPS.]This probably reflects the generally low interest rates on US government debt as the dollar has been one of the strongest relative to other currencies.

In terms of months and level, it is looking long in the tooth, but history also says it is probably pointless to jump out.

Summary: There is a bit more enthusiasm about the economy, but not much. Lower gas prices will lower the GDP metric directly, but Christmas-related buying will probably improve to compensate. No great improvement is expected and, consequently, companies are unlikely to raise hiring or wages much more than they've been doing. Government entities aren't likely to go gang-busters either, but here too voters are a little more willing to approve funding for roads and schools. A "new normal" seems like a good guess: growth, but slow.

Even though the stock-market is booming, it is without excitement: more like "there's no other game in town, while the FED keeps rates low; and, profits are high through cost-control". The divergence cannot go on forever, but it can resolve itself in various ways. Much of the market-sentiment is driven by what John Hussman calls "superstition" about the Fed's ability to keep this playing out for a many more years. The FED continued to say that the turning point is far away, so the game could go on.

The biggest "anticipated wildcards" for 2015 will how the market reacts to the FED, and how the drop in oil-prices filters through (given that a lot of capital investment and employment growth came from the U.S. oil sector). A new downturn -- particularly in the stock market, if not the economy -- is likely before Obama's term ends, but he might squeeze through... and Democrats will have something to brag about.

Comments

Post a Comment